Humira retains its throne as the top-selling drug for the ninth year in a row, showcasing incredible staying power at the tail end of its product lifecycle. AbbVie’s crown jewel is not only record-breaking in its relentless streak as the best-selling drug, but also in its unprecedented breach of the $20bn sales threshold. This behemoth brand is the highest-value pharmaceutical of all time. Unsurprisingly, biosimilar manufacturers have flocked towards the golden opportunity to claim a slice of the pie. There are several FDA-approved adalimumab biosimilars raring to encroach upon Humira’s US market share in 2023.

In the face of such fierce competition looming, AbbVie is lining up promising assets in the autoimmune and

immunology (A&I) space to succeed Humira. In particular, the development of Rinvoq and Skyrizi is integral to AbbVie’s strategy to safeguard its market share, and these products are expected to generate over $15bn in risk-adjusted sales by 2025. The reliance on multiple new revenue streams to offset biosimilar erosion, including these new products plus additional growth from AbbVie’s other therapeutic platforms, highlights that Humira’s phenomenal success is unlikely to be replicated by a single product. In fact, Humira alone constituted a remarkable 43.3% of AbbVie’s net revenues in 2020, and its sales have been the chief driver of the company’s year-on-year growth.

Humira’s outstanding longevity as a mainstay of

treatment for the A&I therapy area is founded upon its broad label addressing eight A&I conditions. This has facilitated physicians’ use of Humira for numerous illnesses within their caseload, consolidating experience and comfortability with the drug. This has allowed AbbVie to concentrate marketing toward targeted specialist personas, building trust and reputation among rheumatologists and gastroenterologists. Furthermore, given that Humira is a costly specialty biologic, AbbVie’s competitive volume-based rebates have crucially gained favor with payers and secured early formulary prioritization, ensuring patient access.

Merck & Co’s Keytruda continues to set records within oncology. In 2019, alongside Revlimid (in third place on this list), it became the first cancer drug to achieve more than $10bn in annual sales, before accelerating a further 30% to achieve its unmatched 2020 total. This is all the more impressive considering Keytruda only made its market debut in 2014, and directly competes with nine other PD-1/PD-L1 inhibitors across various different indications and geographies. Keytruda’s trajectory may see it match Humira’s $20bn peak year potentially as early as 2025.

Supporting Keytruda’s gigantic rise has been the incredible commitment from Merck’s R&D engine. The company lists over 700 clinical trials for Keytruda across the spectrum of oncology, not to mention additional partner or investigator-initiated studies (~850). This is best exemplified by the state of its US prescribing information leaflet, which has ballooned to 97 pages long at the last count. New FDA approvals have prompted Merck to update its label a total of 30 times since that first authorization in advanced melanoma. Continued interest in combination therapy approaches

and potential expansions into new adjuvant settings provide ample opportunity to target new patients, while development work for formulation and dosing regimens will enable commercial longevity.

What is the strategy to navigate through the loss of exclusivity for Revlimid? That is the question investors had been demanding of Celgene management for years, as Revlimid’s proportion of total company sales grew and grew, eventually reaching uncomfortable levels. Rather than face this patent cliff head-on, Celgene instead consented to be acquired by Bristol Myers Squibb, seeking comfort and diversification as part of a much larger organization. The question still remains for the combined organization, as a $12bn product is always going to have an outsized effect on overall strategy and portfolio management.

For BMS, volume-limited settlement agreements with generics manufacturers provide a somewhat cushioned landing and buy time to execute on its wider multiple myeloma and lymphoma portfolio. This includes next-generation products such as the cell therapies Breyanzi and ide-cel. Part of the answer also lies in maximizing Revlimid sales while it is still patent-protected, thus providing a higher base from which erosion begins. 11.9% annual growth is an excellent outcome for 2020, with peak-year sales of around $13bn likely to come in

2021 on account of increased triplet sales and increased duration of treatment, alongside continued uptake in the first-line setting.

Upcoming large-impact catalysts for BMS in hematological malignancies.

Expected date

Drug

Indication

Catalyst title

May 2021

Abecma

Multiple myeloma

CHMP Opinion

Breyanzi

Diffuse large B-cell lymphoma

June 2021

Lirilumab

Chronic lymphocytic leukemia

Phase II w/ Rituximab Results

Aug 2021

Onureg

Acute myelogenous leukemia

Dec 2021

Revlimid

PDUFA for sNDA - RVd 1st Line

Dec 2022

Indolent non-Hodgkin's lymphoma

Phase II TRANSCEND FL Results

Marginal zone lymphoma

Source: Biomedtracker, February 2021

Eliquis has impressively surpassed its competitors and become the anticoagulant of choice despite being the third novel oral anticoagulant (NOAC) to reach the market. The brand commands the largest share of the oral anticoagulant (OAC) market and accrued 16% year-on-year growth in its seventh year since its initial launch in 2013. Eliquis’s share of new-to-brand and total brand prescriptions grew to 61% and 52%, respectively, in Q4 2020. Thus, Eliquis was prescribed at least twice as often as all its fellow NOACs combined: Pradaxa, Xarelto, and Savaysa.

Real-world data have built physicians’ confidence in Eliquis’s efficacy and safety and fueled its remarkable rise to the top of the OAC market. Pivotal data from the US Medicare population pitting Eliquis, Pradaxa, and Xarelto against warfarin in patients with non-valvular atrial fibrillation established Eliquis’s superiority in reducing the risk of stroke by 60% and major bleeding by 49% compared to warfarin. Moreover, Eliquis outperformed Pradaxa, as the latter did not achieve statistically significant reductions in stroke/systemic embolism, and Xarelto, which only reduced the risk of stroke by 28% and was unsuccessful in reducing major bleeding. Bristol Myers Squibb has reaped the rewards of these outstanding data, in addition to further real-world studies, consolidating Eliquis’s best-in-class reputation and fueling its rising demand.

Shielded by sturdy intellectual property, Eliquis will continue to enjoy growth for years to come. In August 2020, Bristol Myers Squibb announced a win pertaining to the US District Court’s decision to uphold both the composition-of-matter (COM) patent (US 6,967,208) and formulation patent (US 9,326,945) covering Eliquis. In light of this and based on settlement agreements with generics manufacturers, Bristol Myers Squibb anticipates generic entry could occur from 2027, during the time window between the expiry dates of the COM (2026) and formulation (2031) patents.

Initially approved as a therapy to treat psoriasis in 2009, Johnson & Johnson’s top-seller Stelara has experienced healthy uptake through label expansions for psoriatic arthritis, Crohn’s disease (CD), and ulcerative colitis (UC). Strong penetration of the inflammatory bowel disease (IBD) market has invigorated Stelara’s sales momentum for a solid performance during the latter half of its growth phase. In particular, Stelara’s use for moderate-to-severe CD (approved in the US in September 2016) has provided the greatest impetus to recent growth, considering that its indication to treat moderate-to-severe UC was the latest addition to its US label in October 2019.

Approvals for both CD and UC have been an important component of success, providing a familiar treatment option for gastroenterologists across these two important patient groups. Stelara possesses a unique mechanism of action in the IBD market as an IL-12 and IL-23 antagonist. Furthermore, its intravenous induction dose elicits rapid responses, allowing physicians to swiftly identify responders and non-responders. Stelara’s high price point also contributes to its substantial revenues, as its annual cost is considerably higher than other biologics in the IBD space. According to the Institute for Clinical and Economic Review’s 2020 report, Stelara’s estimated annual treatment costs for UC reach $91,609 based on average net price to payers per maintenance year.

Stelara’s growth in the UC market will be stunted due to patent expiry in the US, affording the drug a growth period shy of four years. In the US and the EU, its patents expire in September 2023 and July 2024, respectively. With Stelara carrying a 21% growth rate into 2021, J&J will nevertheless look towards maximizing the remaining commercial opportunity in the IBD arena before biosimilars hit the market.

Like many of the other drugs in this top 10 list, Eylea’s ascent up the sales rankings is driven by an impressive clinical dataset and the steady accumulation of new patient populations to target via indication expansions. Unlike the vast majority of others, its developers – in particular Regeneron in the US – have achieved this without resorting to price increases. Its list price of $1,850 per vial narrowly undercuts its rival Lucentis, and this commercial advantage is supported by a favorable clinical profile, enabling less frequent

injections. This is a critical differentiator in the retinal disorders that Eylea treats, as intravitreal injection is required to deliver treatment to the back of the eye.

As the anti-VEGF market developed with clinical trials supporting new indications beyond wet age-related macular degeneration, including diabetic retinopathy, macular edema, and others, Regeneron and its European partner Bayer were in full control of the competitive dynamic. The result was consistent annual

sales growth for Eylea as the class expanded, continually squeezing out Lucentis’s market share. In 2020, this equated to $7.9bn in sales, enough to place this niche eye disorder therapy in sixth place in the best-selling drug list. Over the drug’s lifetime, it has accrued $43bn in cumulative revenues; not quite enough to displace Lucentis, which launched with a full five-year headstart in 2006, although Eylea is expected to also lead on this metric by the end of the year as it continues its upward trajectory.

Once the darling of the PD-1 inhibitor class, Opdivo is now flatlining and its divergence from Keytruda becomes more startling each year. The key turning point was the 2016 failure of Bristol Myers Squibb’s CheckMate 227 study to show a benefit in the strategically important first-line non-small cell lung cancer (NSCLC) treatment setting, contrasting Keytruda’s practice-changing KEYNOTE-024 trial. This result rewrote the narrative between the two drugs, as Merck followed up with additional successes across a range of solid tumors while BMS struggled to define a niche within NSCLC.

Now that Opdivo’s sales growth has stalled, even declining at a slight -1.4% to $7.9bn in 2020, the concern is whether BMS will be able to breathe fresh life into its cornerstone immuno-oncology drug. Keytruda has certainly leapt ahead in the minds of prescribers and potential drug development partners seeking a PD-1 backbone, and this hard-won perception will be difficult to overcome. Nevertheless, a return to growth is expected in line with eventual first-line NSCLC approval and the recovery of cancer patient volumes following the pandemic. The ultimate victor may be decided not by peak-year sales – Keytruda’s

lead is likely unassailable at this stage – but rather commercial longevity and how well each developer can manage their drug lifecycles. For biologics in particular, life does not end post-patent expiry, and BMS still has until 2028 to invest in and shape Opdivo’s long-term future.

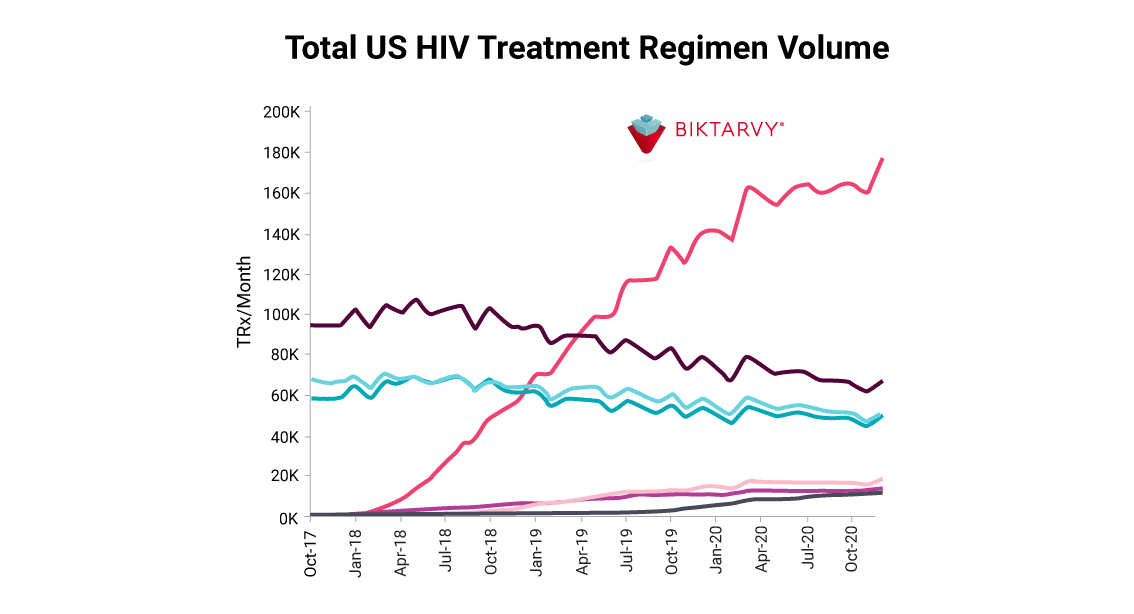

Launching with a clinical dataset that enables gold-standard positioning, first-line recommendation in treatment guidelines, as well as Gilead’s longstanding presence within HIV, Biktarvy rapidly entered the top 10 best-selling drugs list this year. Biktarvy achieved 53% annual growth to reach $7.3bn in 2020 sales, hugely impressive considering its 2018 debut. Gilead has effectively cannibalized its own older HIV products such as Genvoya, but also gained market share through competition with ViiV Healthcare’s Triumeq. In total, half of all HIV patients begin treatment with Biktarvy, and it is the most commonly prescribed regimen in every

major market. This makes Biktarvy one of the most successful launches in history, eclipsed only by Gilead itself and its hepatitis C cures Sovaldi and Harvoni.

Unlike these drugs, Biktarvy is poised to generate multi-blockbuster sales for many years to come, providing Gilead with extremely stable foundations from which to continue its expansion into oncology and potential new therapeutic areas. Datamonitor Healthcare expects Biktarvy to eventually cross the $10bn threshold in annual sales and maintain market exclusivity until 2033. This leaves Biktarvy protected from major competitive

threats, unless there is a drastic shift in how physicians manage chronic virologically suppressed patients. One possible innovation may come in the form of long-acting injections, whereby a subcutaneous injection administered every three or six months improves upon the convenience of an oral once-daily pill. Gilead is initiating late-stage trials of lenacapavir combinations in this setting, while ViiV Healthcare has already launched Cabenuva as a monthly injection of cabotegravir and rilpivirine. Nevertheless, key opinion leaders expect daily oral pills to remain the preferred option for patients.

Biktarvy patient share in the US HIV market. Source: Gilead, February 2021

Xarelto has bounced around the bottom of the best-sellers list for several years, occasionally dropping out, but now occupying its highest position at ninth. The anticoagulant boasts the broadest label of the NOACs as the only one indicated for peripheral artery disease (PAD) and coronary artery disease (CAD) treatment. Additionally, it possesses the advantage of convenient once-daily dosing over Eliquis and Pradaxa. Nevertheless, Xarelto has endured headwinds and resides in the shadow of rival Eliquis’s stellar performance (as the fourth best-selling drug in 2020 and the market-leading anticoagulant). In 2019, Bayer and Johnson & Johnson forked out a hefty $775m to

settle lawsuits for ~25,000 claims centered around the safety risks, including stroke and bleeding injuries associated with Xarelto. Despite investments into the COMPASS and VOYAGER lifecycle management studies for CAD and PAD, its adoption in these segments has left much to be desired.

Generic erosion is set to be staggered across Xarelto’s geographies. Although its US compound patent expires in August 2024, there is potential for further pediatric exclusivity in this market. Moreover, Bayer is placing its hope in a US patent for the once-daily formulation that extends to 2034. Based on a settlement agreement

with Mylan, a once-daily generic may be launched in the US as early as 2027. A longer lifecycle in the US is much needed, considering the dampening effect that substantial rebates in this market have had on Xarelto’s performance. Outside of the US, where recent growth has been sharper, Xarelto faces shorter periods of exclusivity. In Europe, exclusivity is anticipated to last until March 2024 based on the addition of pediatric venous thromboembolism data to Xarelto’s label following supplemental approval in January 2021. In China, Xarelto’s patents expired at the end of 2020, heralding the start of its decline due to generic erosion.

Launching in 2013 as a first-in-class BTK inhibitor, Imbruvica has steadily grown its addressable market via a series of indication expansions across six different diseases, centered around its core use in chronic lymphocytic leukemia (CLL). This slow accumulation of additional approvals and new geographies, as well as the important role it plays within the CLL treatment algorithm, has allowed its developers AbbVie and J&J to nurture impressive and consistent yearly growth. For the first time in 2020, Imbruvica can now be listed among the top 10 best-selling pharmaceuticals in the world. Its $6.6bn in sales are split along geographic

lines; AbbVie reports in the US while J&J records international revenues, with each paying the other a portion of profits.

Unusually for the biopharmaceutical industry, the response to develop follow-on BTK inhibitors has been somewhat muted, especially considering Imbruvica’s sizable commercial footprint. Calquence (AstraZeneca) secured the second FDA approval in the class in 2017, while Brukinsa secured an historic first for a Chinese-developed cancer drug for BeiGene in 2019. Velexbru is additionally available in Japan. Rather than compete

within established oncology indications, next-generation BTK inhibitors are increasingly seeking to apply the mechanism to inflammatory and immunological diseases – following on from Imbruvica’s success in graft-versus-host disease. As the figure below shows, there is intense competition within rheumatoid arthritis and lupus, while Roche, Merck KGaA, and Sanofi all have ongoing Phase III clinical trial programs in multiple sclerosis.