Specialty Drugs Outweighed Traditional Drug Spending For The First Time

Janssen US Net Drug Prices Declined 5.7% in 2020; J&J Pushes Rebate Reform

Sanofi Paid $14.6bn In Rebates In 2020; Net Prices Were Down

Albireo Sets Sights On Rare Disease Model

Novartis Steers Zolgensma Towards Commercial Success In Europe

Coronavirus Vaccines As A Public Good: How Reasonable Is Reasonable?

Some Companies Say 'No' To China's Latest VBP Round

Drugs for inflammatory conditions and cancer drove the increase in spending among the pharmacy benefit manager’s commercial plans, according to a drug trend report from Cigna's Evernorth.

Specialty drugs have been a fast-growing segment of US drug spending for many years, but in 2020 specialty drugs accounted for more than half of pharmacy spend for the first time, according to a drug trend report from Cigna Corp.'s Evernorth. Spending on specialty drugs among commercial plans managed by Cigna's pharmacy benefit manager Express Scripts was 50.8% of pharmacy spend compared to 49.2% for traditional drugs, with drugs for inflammatory conditions, cancer, HIV and rare disease driving the increase.

The report offers a view of US retail pharmacy trends based on spending by commercial insurance plans through Express Scripts, which has long released the report. Evernorth is the new brand name Cigna introduced last year for its health services portfolio, including Express Scripts, Accredo, eviCore and Freedom Fertility.

"While drugs to treat rare and specialty conditions were used by less than 2% of the population in 2020, they accounted for almost 51% of spending under the pharmacy benefit," the report said. Additionally, 17 of the top 25 drugs ranked by total pharmacy spend were specialty medications in 2020.

Exhibit 1. Top Drugs By Spending For Express Scripts Commercial Plans 17 of the top 25 drugs ranked by total pharmacy spend were specialty medications in 2020

Total average drug spending across commercial plans with pharmacy benefits managed by Express Scripts – about 27.3 million lives – increased 4% in 2020, with 3.1% of the growth coming from utilization increases and 0.9% coming from unit cost, Evernorth said. Express Scripts mitigated unit costs to under 1% through rebates with drug makers and by drug utilization management programs that focus on more affordable medications, including shifting to generic drugs when available.

In a sign that payers are looking for new ways to manage the rising cost in specialty areas, Cigna is testing a pilot program this year targeting patients loyal to Novartis AG' Cosentyx (secukinumab), offering eligible patients a $500 debit card to switch to Eli Lilly & Co.'s Taltz (ixekizumab) or other preferred drugs. (Also see "Cigna Switch Program Intensifies Competitive Dynamics For Cosentyx" - Scrip, 6 Apr, 2021.)

From 2016-2020, the list price for commonly used brand drugs has increased 36%, while the price for commonly used generic drugs has decreased 42%, Evernorth said. In the debate over drug prices, drug manufacturers have countered for several years that list prices do not accurately reflect the way brand drug prices are offset by manufacturer rebates to result in lower net prices.

PBMs like Express Scripts are part of the problem, the industry has argued, because they absorb the savings from rebates and it is not always clear how those savings are directed. PBMs and insurers say the savings are used to lower the cost of insurance premiums. Much of the policy debate around drug prices has been around rebate reform that would pass the savings from rebates onto patients directly.

Newer biologic drugs for inflammatory conditions like psoriasis, atopic dermatitis and ulcerative colitis have been a contributing driver of pharmacy spending in recent years. In 2019, Express Scripts reported that commercial health plan spending on drugs for inflammatory conditions grew 17.1%, driven by drugs like Cosentyx, Taltz, Regeneron Pharmaceuticals, Inc./Sanofi's Dupixent (dupilumab) and AbbVie Inc.'s Skyrizi (rixankizumab). (Also see "High-Priced Entries Drive 17% Rise In Spending On Anti-Inflammatory Drugs" - Scrip, 28 Feb, 2020.)

In 2020, spending growth increased again by double digits, with spending on drugs for inflammatory conditions up 15.6%, including an 11.1% increase driven by unit cost and 4.5% for utilization. Specialty injectable medications account for nearly 95% of medication spend in the therapeutic area, Evernorth reported. The average cost per prescription for specialty drugs for inflammatory conditions is $4,500.

Evernorth forecasts increases in drug spending for inflammatory disease drugs is expected to continue through 2023, due to expanded indications for existing therapies and the potential launch of new drugs. In 2023, AbbVie's blockbuster Humira (adalimumab) is expected to face its first biosimilar competition in the US, which could significantly lower spending for the therapeutic area.

Cancer drugs were another driver of specialty drug spending, with 12.6% spending growth in the category, including 6.8% driven by unit cost and 5.8% by utilization. Many of the drugs are new or are for new indications. Nearly 40 new cancer drugs were approved in 2019 and 2020, often for rare cancers with relatively small patient populations, Evernorth said.

Evernorth expects costs and utilization in cancer will continue to grow for the next few years due to increased cancer diagnosis and patients living longer due to the effectiveness of current therapies. Generic launches, including for Bristol Myers Squibb Company's Pomalyst (pomalidomide) for multiple myeloma and Pfizer Inc.'s Sutent (sunitinib) for renal cell carcinoma, could offset the growth in 2022-2023.

HIV was another growth category with drug spend up, a 5.3% increase driven by both utilization and cost. Generic availability of Gilead Sciences, Inc.''s Truvada (emtricitabine/tenofovir disoproxil fumarate) for pre-exposure prophylaxis (PrEP) helped to decrease unit cost growth of 3.8%. Evernorth forecasts that HIV drug spend will remain at or slightly above 6% through 2023, when generic launches of ViiV Healthcare's Selzentry (maraviroc) and Johnson & Johnson's Prezista (darunavir) could help offset the cost of newer launches.

Gilead's Truvada lost exclusivity in October 2020, but Gilead has been able to offset some of the losses with growth of Descovy (emtricitabine/tenovovir alafenamide) for PrEP.

Some drug categories offset increased spending in areas like inflammatory disease and cancer. One area was pain and inflammation, which declined 20.3%, partly due to a 10.3% decline in opioid utilization. Another was antihypertensives, which declined 5.3% despite a 4.3% increase in utilization. Generic drugs made up 98.7% of the market in 2020, but 17 out of 100 people take antihypertensive medication, Evernorth said, accounting for 2.1% of total spend in 2020.

The report by Evernorth also looks at some of the trends impacted by the COVID-19 pandemic, including how the virus impacted new patient starts. (Also see "COVID-19 Hit New Medication Starts Across Broad Therapeutic Areas" - Scrip, 7 Apr, 2021.)

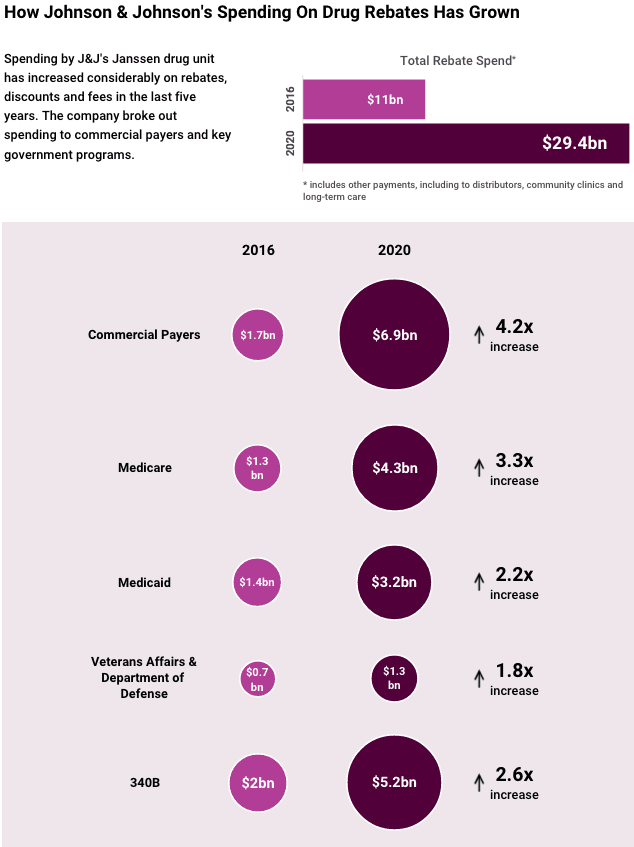

Janssen's net drug prices declined for the fourth year in a row in 2020, while list prices increased 3.8%, according to the company's drug pricing report.

Johnson & Johnson's US net drug prices declined for the fourth consecutive year, down 5.7% on average across the portfolio, the company said in its annual drug pricing transparency report. Pointing to years of net price declines across the US drug portfolio, J&J used the platform to push for US drug price reforms that direct savings from rebates to patients rather than pharmacy benefit managers (PBMs).

The compound annual net price of the medicines sold under its Janssen drug unit has declined 14.4% since the beginning of 2016, the company said in a recent report, although US list prices consistently increased during that period. US list prices across the entire J&J portfolio increased 2.8% in 2020, the lowest level of increase in five years.

List prices were offset with rebates to payers in formulary negotiations as is typically the case in the sales of pharmaceuticals. Government programs also require certain discounts and rebates. Those amounted to $29.4bn in 2020, including rebates, discounts and fees, totaling as much as 53% of the list price of its drugs, J&J said.

"Since 2016, the first year covered by a Janssen US Transparency Report, the rebates and discounts we provide have nearly tripled, reflecting payers' growing negotiating power," the company said." Indeed, in J&J’s first drug pricing report released in 2016, the company said it spent $11bn on rebates, or about 35.2% off the list price. (Also see "Janssen's Drug Pricing Report Emphasizes Value Of Rebates" - Pink Sheet, 28 Feb, 2017.)

The company highlighted its spending increases under commercial plans but also across government programs, including Medicare, Medicaid and Veteran's Affairs.

The company blamed payers and specifically PBMs for driving an increasingly untenable situation for drug prices.

"Three PBMs currently cover 256 million Americans – more than 2/3 of the US population – and handle 74% of prescriptions processed in the US," the company said. "Further, the number of unique medicines not covered (that is, placed on 'exclusion lists') nearly quadrupled from 209 in 2016 to 846 in 2020." The statistics highlight the influence of steep rebates on formulary placement as drug makers use rebates to negotiate for prime real estate on formularies.

J&J's latest drug pricing report echoes a sentiment that has been coming from industry for about five years – that attacks on high US drug prices do not account for the current market dynamics around rebates and formulary negotiations. Drug price reform should focus on changes to the rebate system and ways to get the savings from rebates directly to the patients who use the medicines, industry has argued. Payers say rebates go toward lowering insurance premiums, but the allocation is not transparent. A big policy push to eliminate rebates was scuttled in 2019 after the Congressional Budget Office determined it would increase spending on Medicare and Medicaid. (Also see "Pharma's Big Defeat: US Rebate Proposal Hits The End Of The Road" - Scrip, 11 Jul, 2019.)

Several big pharmas have committed to releasing annual drug pricing reports in an effort to improve drug pricing communication with the public. As rebates have steadily increased in recent years, the case has grown more beneficial for pharma to make that information public.

Source: The 2020 Janssen US Transparency Report

Sanofi released its most recent annual drug pricing report in March, in which it outlined a similar dynamic. The company said it paid 54% of its gross sales in rebates in 2020, or $14.6bn; it was the third year the company paid more than 50% of gross revenue in rebates. Sanofi's US average net prices decreased 7.8%, while aggregate list price across the commercial portfolio increased 0.2% in 2020. (Also see "Sanofi Paid $14.6bn In Rebates In 2020; Net Prices Were Down" - Scrip, 3 Mar, 2021.)

As drug price reform continues to loom under a Democrat-led Congress, the industry has been focusing on reforms that impact patient affordability, a serious concern in the US. J&J, in its report, said two key issues are that rebates are not passed directly to patients and insurers base patient cost-sharing on list prices, not net prices.

High cost-sharing also impacts how medicines are used, since higher costs lead to higher rates of prescription abandonment, as much as 69% when patient costs exceed $250 for a prescription, compared to just 8% when costs are $10 or less, J&J said, citing data from IQVIA. This, industry argues, can result in higher overall health care spending due to increased doctor visits or hospitalizations.

J&J also took the opportunity to argue against reforms that would benchmark US drug prices to international reference pricing, repeating frequent industry arguments. "International reference pricing would, in essence, give control of part of the US health system to other countries and subject US citizens to the consequences of political decisions made in another country," J&J said. "It would hinder the development of new treatments, creating a potential vulnerability for response to future pandemics and could reduce the nation's overall global competitiveness in an essential industry."

The company also highlighted biosimilars as a contributor to US savings on drug spend – exploring its experience with Remicade (infliximab) specifically. The launch of multiple biosimilar competitors has reduced the price of the product since the first one launched in 2016, the company pointed out. Pfizer Inc.'s Inflectra (infliximab-dyyb) was the first biosimilar version of Remicade to reach the market and only the second biosimilar to be approved in the US. (Also see "Many Firsts As Celltrion/Pfizer’s Inflectra Becomes Second US Biosimilar" - Scrip, 5 Apr, 2016.)

Ironically, Inflectra and other infliximab biosimilars that followed were slow to gain traction, raising concerns the market for biosimilars in the US could fizzle. To compete, J&J took a hit on the price of Remicade by offering steep rebates to payers, which ultimately stuck with the branded product because of the high volumes and rebates. Pfizer filed a lawsuit against J&J over the marketing practices in 2017, calling them anti-competitive. (Also see "Pfizer v. J&J Sets Stage For Biosimilar Showdown Over Exclusive Contracts" - Pink Sheet, 20 Sep, 2017.)But after lowering the price of Remicade, J&J argued that the availability of biosimilars still contributed to health care cost savings. Today, there are three biosimilar versions of Remicade on the market, including Merck & Co., Inc.'s Renflexis, which launched in 2017, and Amgen, Inc.'s Avsola, which launched in 2020.

The average sales price (ASP) of Remicade, calculated by the Centers for Medicare & Medicaid (CMS), has come down from $782 in 2016 to $410 in 2020, the company said.

The company released an annual pricing report, showing that Sanofi's US average net prices declined for the fifth year in a row.

Sanofi returned 54% of its gross sales to payers through rebates in 2020, marking the third consecutive year the company paid more than 50% of gross revenue in rebates. The French pharmaceutical company released its fifth annual pricing report on

3 March, fulfilling a commitment by the company to be more transparent about drug pricing.

The top-line takeaway from the report is that Sanofi's US average aggregate list price across the commercial portfolio increased 0.2% in 2020, while the US average net price decreased 7.8%. Sanofi said it is the fifth consecutive year US net prices have declined on average, though in 2019 net prices declined by more,

11.1%. Net prices reflect the impact of rebates and discounts off of the list price. The aggregate list price increase of 0.2% was the lowest increase in at least five years.

The company also revealed that it paid a total of $14.6bn in rebates in 2020, including $5.9bn in mandatory rebates to governments and $8.7bn in discretionary rebates. That underscores one of the

industry's longstanding arguments when it comes to the issue of drug pricing – that drug makers heavily offset price increases through rebates, but those price concessions do not trickle down to the patient.

The narrative is one the drug industry has tried to move into the forefront in the last five years as drug pricing has become a hot button issue with the public and politicians, particularly in the US. (Also see "Drug Pricing: PhRMA Report Aims To Shift Focus To Supply Chain" - Pink Sheet, 19 Jan, 2017.) Drug makers have tried to point the finger at pharmacy benefit managers and health care plans while promoting rebate reform as a key element of legislation to address US drug pricing issues. The effort took a big hit in 2019. (Also see "Pharma's Big Defeat: US Rebate Proposal Hits The End Of The Road" - Scrip, 11 Jul, 2019.)

Several big pharmas committed to releasing annual pricing reports several years ago as part of a strategy to be more transparent about price; the reports also present an opportunity for companies to highlight how much they offset annual drug price increases with rebates. (Also see "Signs Of Change? Lilly, Merck, Janssen Report Slowing List Price Growth In 2018" - Scrip, 25 Mar, 2019.)

Compiling average aggregate portfolio price increases doesn't always tell the whole story, however, as companies might put more substantial price increases in place for a newer high-growth brand while significantly lowering the price on a mature brand facing generic competition for the first time.

Sanofi has committed to limit total annual list price increases in one year to a level at or below the projected growth rate for the National Health Expenditure (NHE) that year, estimated and published annually by the Centers for Medicare & Medicaid Services (CMS). (Also see "Sanofi's Drug Pricing Pledge Ties Increases To National Health Expenditure" - Pink Sheet, 9 May, 2017.)

The NHE projected growth rate was updated to 5.2% in March 2020. Sanofi increased the list price of 50 out of 80 medicines in 2020, all of which were within the pricing guidelines, the firm said.

If the company does take a price increase above the NHE growth rate for a medicine that results in a list price increase greater than $15 for a full course of treatment per year, the company vowed to outline the rationale and the clinical value.

Sanofi called out one of its recent approvals in an attempt to outline the value – Sarclisa (isatuximab), which was approved in the US in March for relapsed/refractory multiple myeloma. SC141760 The drug had a wholesale acquisition cost (WAC) of $650 per 100mg vial and $3,250 per 500mg vial, a price the company said that for a full year of therapy for a typical patient weighing between 70kg-80kg (154lbs-176lbs), including a standard infusion cost, was less at launch than the rival anti-CD38 treatment Darzalex (daratumumab), marketed by Johnson & Johnson.

Sanofi highlighted one significant price decrease on Lovenox (enoxaparin) as well, a mature franchise which had a 71% price drop in October. Generic versions of Lovenox are available in the US, though the product still generated €1.35bn in 2020, with sales coming primarily from outside the US and also benefiting from recommendations to use heparin in COVID-19-hospitalized patients.

Sanofi has highlighted the declining prices of its insulins in past reports and how those reductions have not made their way to patients. (Also see "Rhetoric Doesn't Square With Reality, Sanofi Drug Pricing Report Says" - Scrip, 5 Mar, 2020.) Diabetes has been a notably charged therapeutic area when it comes to discussion about drug pricing and patient affordability given the chronic long-term nature of the disease and the fact that insulins are older medicines that patients nonetheless pay heavily out of pocket for.

This year, Sanofi said the US net price of its insulins has declined by 53% and the net price of its top-selling insulin Lantus (insulin glargine) 100 units/mL has fallen by 44.9% since 2012, but that average out-of-pocket costs for patients with commercial insurance and Medicare have increased by approximately 82%. List price increased 141% from 2012 to 2020, although it appeared to plateau in 2020.

"Despite the rhetoric about skyrocketing insulin prices, the net price of insulin has fallen for six consecutive

years, making our insulins significantly less expensive for insurance plans," Sanofi said. That decline in price has not resulted in a corresponding reduction in patient out-of-pocket costs, however.

"Health plans are placing more of the cost burden onto patients through high deductibles, coinsurance and multiple cost-sharing tiers," Sanofi said.

"It is clear that focusing solely on the list price of medicines will not guarantee that patients will be able to get and afford the medicines they need," the company said.

Sanofi has deprioritized diabetes as a therapeutic area in favor of areas like cancer and immunology as its insulin brands have matured and as the competitive dynamics and pricing pressure in diabetes have intensified. (Also see "Sanofi, Long-Time Leader In Diabetes, Is Exiting Diabetes Research " - Scrip, 10 Dec, 2019.)

Anticipating approval this summer of the first drug for PFIC, Albireo hopes to add Alagille syndrome and biliary atresia to odevixibat labeling. Firm has modeled its commercial plans on the success of other rare disease firms.

By modeling its commercial plans on other companies’ successes with rare disease drugs, Albireo Pharma Inc. thinks it can eventually derive blockbuster annual sales from lead candidate odevixibat, which is under US Food and Drug Administration review for approval to treat progressive familial intrahepatic cholestasis (PFIC) but is also in late-stage development for other cholestatic liver diseases.

Odevixibat, a selective, oral ileal bile acid transporter (IBAT) inhibitor, has a 20 July action date at the FDA, and the firm already has Phase III registrational trials under way in Alagille syndrome and biliary atresia.

During an investor presentation on 11 February, CEO Ron Cooper and other Albireo executives detailed plans to gradually build odevixibat to $1bn in sales in the US and EU, by trying to replicate the success of Alexion Pharmaceuticals Inc. with Soliris (eculizumab), Vertex Pharmaceuticals Incorporated with Kalydeco (ivacaftor) and Biogen, Inc. with Spinraza (nusinersen). Alexion’s success with Soliris and the follow-on drug Ultomiris (ravulizumab) drove the company’s $39bn buyout by AstraZeneca PLC in December. (Also see "AZ's Alexion Acquisition Looks Astute Bit Of Business" - Scrip, 13 Dec, 2020.)

Odevixibat is poised to become the first drug approved for PFIC in both the US and Europe, with both regulatory decisions expected this year. (Also see "PFIC Space Hots Up With Albireo and Mirum Filings" - Scrip, 9 Dec, 2020.) Foster City, CA-based Mirum Pharmaceuticals, Inc. is battling Albireo for first-to-market status in PFIC and also Alagille syndrome with maralixibat, an apical sodium-dependent bile acid transporter (ASBT) inhibitor it licensed from Shire Pharmaceuticals Group PLC in 2018. (Also see "Mirum’s Long-Term Alagille Data Support Case For Early Filing" - Scrip, 28 Nov, 2019.) Maralixibat has a 1 October user fee date for Alagille syndrome.

In a 16 February note, WedBush analyst Liana Moussatos predicted that odevixibat would be first approved in PFIC and a “fast follower” to maralixibat in Alagille syndrome, with Albireo also likely to obtain first approval in biliary atresia.

“We see a high likelihood for approval of odevixibat in PFIC on or before the July 20, 2021, PDUFA date with a broad label in all three genetic subtypes and project gross worldwide sales of more than $700m in 2028,” Moussatos said.

Mirum’s maralixibat was filed for EU approval last November based on Phase II data in PFIC2, but not the other two subtypes. The company has a rolling new drug application under way for the indication at the FDA.

“In our view, odevixibat’s best-in-class clinical profile and likely first-to-market advantage positions it to potentially become standard-of-care for PFIC and possibly in other cholestatic liver diseases,” the WedBush analyst added.

Jefferies analyst Eun Yang said in an 11 February note that Albireo’s goal of aggregating blockbuster revenues across three indications with odevixibat is “quite reasonable.” To do this, the Boston-headquartered firm would need to have about 5,000 patients on therapy of an estimated 18,000 addressable patient population, Yang said.

Albireo’s goals and expectations, however, are based on a revised patient population projection of about 100,000 possible patients across the PFIC, Alagille and BA indications, Cooper told Scrip.

“We believe that the ex-US opportunity is large,” he said. “If you look at Spinraza and Soliris, these are products that in their second year of launch more than 50% of their sales came ex-US. We believe in total there’s 100,000 patients that could be available to odevixibat. Our plans are to commercialize in the US and Europe because it’s a highly concentrated audience. These physicians are at tertiary centers – we only need about 10 representatives [apiece in the US and Europe] and not that big of an infrastructure.”

Cooper pointed to the commercial experience of his team – his two-plus decades at Bristol Myers Squibb Company, chief commercial officer Pamela Stephenson’s decade each at Pfizer Inc. and Vertex and chief financial officer Simon Harford’s roughly three decades of experience at both Eli Lilly and Company and GlaxoSmithKline plc – as evidence of the likelihood of Albireo getting the transition from clinical-stage to commercial company right.

For the rest of the world, Albireo is talking to potential partners, and recently signed a deal with Medison Pharma Ltd. to market odevixibat in Israel. “When we think about the other parts of the world, we don’t want to get ahead of ourselves,” Cooper said. “There are some pretty big opportunities in the Middle East and in parts of Latin America.”

Following the examples set in rare disease commercialization by companies like Alexion offers a lot of analogous situations, the CEO said – addressing an ultra-rare disease population and an unmet medical need can help with refining a go-to-market plan. “The disadvantage is nobody has brought a drug to the world for PFIC, so the specificity for PFIC and cholestatic diseases is an unknown right now,” he admitted. “But we think we’ve mitigated that as much as possible with really global market research and looking at those analogs.”

The pivotal PEDFIC1 study of odevixibat is the only prospective, randomized and placebo-controlled Phase III study in cholestatic liver disease presently, Cooper said, and Albireo anticipates that that will give his company a head start in reimbursement talks with US insurers and government agencies in the EU. A potential complication is the UK’s recent exit from the European Union; Albireo anticipates that a mutual recognition process between the EMA and the UK health care system will largely take care of approval, and the company always expected to have UK-based infrastructure for commercializing odevixibat.

Chief commercial officer Stephenson said Albireo has also approached its pricing strategy and pre-approval talks with reimbursement officials with an eye to what has worked previously for other rare disease therapies. “What we know about pricing and in particular in rare disease is that payers look for a high unmet need, a high burden of disease, … robust clinical evidence from Phase III studies to demonstrate the clinical benefit to patients and they want to understand the cost offsets,” she said. “All of those together lead us to think that these analogs in rare disease like Spinraza, Soliris, Kalydeco, are in the price range that odevixibat should be based on these factors.”

This indicates odevixibat pricing might be in the range of $300,000-$500,000 a year, according to WedBush’s Moussatos, although Albireo did not offer any specific pricing range during its 11 February presentation. CFO Harford said that if odevixibat reaches the blockbuster threshold as expected, the firm anticipates about 60% of sales in the US and 40% ex-US. PFIC is expected to yield about 30% of sales, with BA bringing in 45% and Alagille syndrome 25%, he added.

Albireo thinks a key differentiating factor for odevixibat in all the indications it is pursuing will be better safety and tolerability than typically seen in the IBAT inhibitor class. (Also see "Albireo Making Headway In Rare Pediatric Liver Diseases With IBAT Inhibition" - Scrip, 25 Oct, 2017.) Even though PFIC is considered the smallest economic opportunity among odevixibat’s first three indications, the company wanted to pick an indication where it perceived a high chance of demonstrating efficacy while also showing a better tolerability profile regarding gastrointestinal symptoms, Cooper explained.

“We’ve always believed that odevixibat would be a great drug for cholestatic liver diseases but we wanted to make sure that we would be successful with the first Phase III study,” he said. “The nice thing about PFIC as a disease is it really is just a disease of bile acids in the wrong place, in this case in the liver. We knew that odevixibat could reduce bile acids effectively, but we didn’t know exactly what would be the right dose and if we were able to do that without causing a lot of diarrhea, because that’s the challenge with IBAT inhibitors.”

In PEDFIC1, the company demonstrated that odevixibat can both reduce bile acids and improve pruritus – the primary efficacy endpoints required for PFIC by the EMA and FDA, respectively, with a relatively low incidence of diarrhea, Cooper said. In addition, that study helped Albireo work out dosing determinations for the pivotal studies in Alagille syndrome (ASSERT) and BA (BOLD). The firm expects Phase III top-line data from ASSERT in 2022 and from BOLD in 2024.

With the EMA and the FDA preferring different primary endpoints in PFIC, Albireo’s top priority was working out a Phase III plan with both agencies so that it would need to conduct only a single pivotal study. Albireo is also conducting the ongoing Phase III PEDFIC2, an open-label extension study to provide long-term data in PFIC patients.

“As you’re doing orphan drug development, often there’s no natural history, the endpoints are often not well defined,” Cooper pointed out. “We worked collaboratively with both the FDA and the EMA to find a trial design that works for both of them. Our main objective was to do one study [because] given the nature of the disease, it would be difficult to do two studies. That was our biggest focus. The fact that we were measuring bile acids for one and pruritus for the other actually was secondary because we always had great confidence that odevixibat had a positive impact on both of those things.”

The head of Novartis Gene Therapies in Europe tells Scrip that innovative payment models and involving all stakeholders have helped payers see beyond a simple price tag and see the benefits of a one-time gene therapy for spinal muscular atrophy.

It has been a very successful week for Novartis AG in expanding access to its gene therapy Zolgensma, with England, Scotland and Italy agreeing reimbursement for the costly spinal muscular atrophy (SMA) therapy, a result of the company's efforts to highlight the value of innovative one-time therapies.

That is the view of Mike Fraser, general manager of Europe, Middle East and Africa at the Swiss giant's Novartis Gene Therapies unit, who spoke to Scrip about the challenges of approaching payers and asking them to cover the world’s most expensive drug, Zolgensma (onasemnogene abeparvovec). "You're bringing something completely unique to the marketplace, a one-time injection with a lifetime of benefits which is something that, as an industry, we're not used to doing, we normally talk of products you take every day or every week or every month," he said.

How to evaluate the value of Zolgensma "was something that was initially one of our biggest objectives," Fraser said, "so we pulled in people that could help us, the usual suspects obviously, like doctors, patients and patient advocacy groups, but also health economists, people that could understand and help explain value over time. It's not rocket science but we actually got those stakeholders together and started to educate, educate, educate, working together.

Mike Fraser, Novartis

The clinical profile of Zolgensma has helped the conversations, he argued. "The first time I saw the very first Kaplan-Meier curve, which showed 100% survival, I said, 'Well, where's the active treatment? The line is missing.' And it was missing because it was superimposed on the 100% line."

Cost-effectiveness agencies in Europe have been persuaded of Zolgensma's value. This week, the English and Scottish health technology appraisal bodies NICE and the Scottish Medicines Consortium gave the green light to the drug, which comes with a list price of €1.79m ($2.13m) but is being offered at what NHS England said was a “substantial confidential discount.”

NHS England CEO Sir Simon Stevens said the agency "has moved mountains to make this treatment available, while successfully negotiating hard behind the scenes to ensure a price that is fair to taxpayers.”

Fraser said, "I must give credit where credit is due to the NHS and NICE: they've been very open and welcoming of us to come and talk to them. We had frank discussions of where we were and where they were and we realized we needed to find a common ground, you've just got to find the right pathway."

That pathway in England was NICE’s Highly Specialized Technologies program, which is intended for ultra-rare conditions. "We were very thankful we got included and obviously we always thought we needed to be included onto that pathway...with any rare disease product at the beginning, you have limited data so you have to use that to hypothesize and extrapolate. But the data was so overwhelmingly convincing, it helped us a lot," Fraser said.

As for the rest of Europe, Novartis has this week achieved national reimbursement for Zolgensma in Italy, "another big payer that is seeing the value of the product through a typical health technology assessment," he noted. In France, Zolgensma is available through the ATU (temporary authorisation for use) framework and discussions are ongoing in that country, as well as in Spain, for wider coverage.

"We've struck early access deals so that we can enable availability while we are talking to the health authorities to allow them to go through their standard process," Fraser said. The agreements being discussed are not exactly same as the NICE/NHS England accords, "but they are very similar in structure. We have been open to innovation in terms of different payment models and in some cases we are working with annuities, where people can pay over time. There are unique differences in each country and it's been great that they're open to it. It's also meant that we've had to change the way we work so we're able to offer these bespoke solutions."

In December, the German pricing and reimbursement authority, the G-BA, suspended the abridged orphan benefit assessment of Zolgensma, stating that it must now undergo a full benefit evaluation to compare the product against other treatments for SMA, such as Biogen, Inc.’s Spinraza (nusinersen) as sales of the one-time therapy exceeded the maximum permitted one-year threshold of €50m. Fraser pointed out that "the problem is, once again, the laws have been built for yesteryear, for products in the past. It's very difficult for a product that's selling on an infrequent basis to achieve €50m a year" but with a product like Zolgensma, "you're going to reach that number quickly." (Also see "Zolgensma Loses Orphan Benefit in Germany After 'Very High Sales'" - Pink Sheet, 10 Dec, 2020.)

Nevertheless, he stressed that "we are working super closely with the G-BA to come up with what's going to be appropriate but in Germany, all the patients have access to the product today."

Reimbursement negotiations during the pandemic have presented particular problems "and getting to the right people has sometimes been a challenge, because a lot of these health authorities have a huge issue on their hands with COVID, but I must say from our point of view, we've been very fortunate in Europe with the access we've had," Fraser added.

He concluded by saying that "the news coming out of the UK and Italy is going to snowball and accelerate other countries to jump onboard because everyone wants to be a part of this. We will see the first commercially successful gene therapy and it provides encouragement to the industry to continue to work in the space and I'm hopeful that others will come into the space."

During a recent press briefing, health officials in China disclosed the country is poised to reach an annual production capacity of 610 million doses for coronavirus vaccines. But they said prices must be based on manufacturing costs and not driven by supply and demand.

A Chinese health official has called upon the nation's developers of COVID-19 vaccines to make sure the prices of their products are reasonable and “affordable to the public.”

Zhongwei Zheng said during a press briefing that, although the prices will be up to each manufacturer to decide, two main principles must the followed. One is the "public good" nature of the vaccines, which means prices should be based on cost not demand and supply, and secondly, manufacturers should consider the public’s willingness to receive them.

In his comments, Zheng pointed to the relation between price and the public’s intention to get vaccinated, which could drive up demand. Domestically developed coronavirus vaccines must be “affordable to the public” in China, the official declared.

Although each developer can set prices, the unique public health nature of the vaccines mean it is widely believed these will be priced in a way to make regulators happy, as well as to cover R&D and manufacturing costs.

As a result, it seem unlikely the vaccines will join their novel biologic peers, which in China have cemented pricing power through premiums over R&D and patent costs. That will not only limit each company’s pricing flexibility for coronavirus vaccines but also profitability.

One way for developers to recuperate costs might be through bulk procurement contacts, which a government usually uses in a public health crisis to ensure public supplies. But so far, the Chinese government has not signed any such purchasing contracts with any companies, leaving people wondering if the vaccines will be so modestly priced that people will want to get vaccinated even without a public procurement scheme.

So far, Chinese firms are working on four front-runner candidates, two from state-owned China National Biotec Group (CNBG) and one each from privately-owned CanSino Biologics Inc. and Sinovac Biotech Ltd. All are in final Phase III development, including at sites outside China, and the CEO of CNBG Xiaoming Yang said recently that his group's products, based on an inactivated virus, are within “last kilometer” before becoming a success.

CanSino’s Ad5-nCoV is based on an adenovirus platform and SinoVac’s CoronaVac uses an inactivated virus.

Flu vaccines provide the most likely model for COVID-19 pricing and distribution in China.

Unlike in the US, where regular citizens can receive flu shots by going to a clinic and being covered by their insurance or employer, China has not rolled out mass immunization programs for flu. People must pay out-of-pocket and go to a designated hospital or clinic, meaning the process is awkward, information lacking, and costs such that many simply won’t bother getting a seasonal flu jab.

Given the urgency and huge massive health need for coronavirus vaccines, if these will indeed be of a self-pay nature, how big the actual public demand in China will be is still a large question mark.

The government hopes that a low price point will drive up demand and encourage those who need them to get vaccinated, by making them widely accessible. But if prices are set too low, producers will have less room to maneuver if they seek to get the product included on the National Reimbursement List, a process which usually cuts original prices by more than 50%.

As many as 100,000 people in China have already been inoculated under various emergency programs, and in the eastern city of Shaoxing people can receive a

vaccine by paying CNY200 ($29), although many locals believe this price tag is too high.

Pricing aside, there are also concerns about the manufacturing and distribution of the vaccines. China’s CNBG said its annual capacity alone could reach one billion doses by 2021, showing its ability to meet potentially large demand. Vaccines usually require cold-chain logistics, easily adding to the costs of storage, transportation and distribution.

In 2019, when China implemented its first Vaccines Administration Regulation, developers were required to have their own manufacturing facilities, while distributors must have the necessary cold chain systems to manage temperature-sensitive vaccines.

Whether CNBG, CanSino or SinoVac can price their COVID-19 vaccines to be both affordable and sustainable will largely depend on their scale, cost structures and technical challenges.

Some observers predict that CanSino’s adenovirus vaccine will be priced higher due to different and more demanding technical requirements.

Only three of 40 qualified international drug firms won in the latest round of China's central bidding process, showing a toughening environment. But some companies are seemingly determined not to lower prices any further.

In China, there is a saying about falling drug prices for off-patent drugs selected for the country's centralized procurement scheme - “there are only lower bids, no lowest prices.”

But given the results from the latest round of volume-based procurement (VBP), as it formally called, some prices are falling so fast that several companies have simply chosen not to budge on their levels.

In a sign deemed by many as a protest, some originators chose to bid with seemingly impossibly high prices, as a way of indicating their unwillingness to lower prices any more. On 20 August, the VBP coordinating authority, the Shanghai Procurement Office, released the results of the latest round of the scheme.

This selected 56 products, many of them widely used cardiovasculars including valsartan, for which the original is Novartis AG’s Diovan, along with captopril, antidiabetic metformin and CNS drug memantine, among others.

Before the round, multiple producers including Novartis had voiced caution about the potential impact on product sales in China, now the second-largest pharmaceutical market in the world (Also see "As China Volume Purchase Builds, Novartis Scrambles To Launch New Products" - Scrip, 24 Jul, 2020.).

In the new round, captopril and metformin attracted the most bidders, resulting in the steepest price reductions given the intense competition. To win the process, makers of the two drugs had to cut their prices by 62-95%, much higher than the average price reduction of 53% across the board for all 56 drugs this time.

China initiated the first round of VBP in 11 major cities - the so-called “4+7” scheme - in 2019 and eventually rolled it out nationwide, and the current round is the first to be implemented in a row. The products chosen for centralized purchasing were also expanded from an initial 25 products to the 56 now.

The obvious winners so far are large-scale domestic firms. Qilu Pharmaceutical Co., Ltd. and Shijiazhuang Pharma topped the list with the most winning bids, which can be attributed to their aggressive price-lowering practices. The companies accounted for four and two of the 10 lowest-priced drugs, respectively.

In comparison, originators had one of their worst rounds so far, with only three out of 40 qualified international drug firms managing to win VBP bids this time. This is in stark contrast to the last round, in which several MNCs had winning bids (Also see "China Still Alluring? AZ, Pfizer Feel COVID Pinch, New Pricing Scheme Clouds Outlook" - Scrip, 6 Aug, 2020.).

Japan's Eisai Co., Ltd. was one of the winners, for vitamin B preparation mecobalamin, while Pfizer Inc. won for its antibiotic linezolid, by lowering their bidding prices by 76% and 90%, respectively, compared to the highest allowed bid prices.

But compared to the first round, in which many companies didn’t participate, and the second round, in which many participants actively cut prices to win, this round saw several manufacturers offer bids that were seemingly too high to even be considered.

Some were at such high levels that they had some wondering if it was a way of effectively saying "no". Merck KGaA, for one, offered metformin at CNY1.40 ($0.20) per tablet, compared to the required highest bid of CNY0.34, while Pfizer put in Viagra (sildenafil) at CNY58.70, above the allowed limit of CNY48.0. AstraZeneca PLC offered Seroquel (quetiapine) at CNY7.0 per tablet, compared to the limit of CNY2.30.

Additionally, Eli Lilly and Company, Johnson & Johnson’s local subsidiary Xian Janssen and Merck & Co., Inc. also offered their drugs with bid prices above the highest allowed levels.

Unwilling to lower prices to the floor and thus with no hope of winning, the obvious tactic indicated that some companies simply chose to walk away instead of participating, analysts said. “Multinational drug makers are setting up a new decision-making model for their off-patent drugs, meanwhile keeping a product portfolio balance,” said Song Yang at Xinda Securities in a 20 August seminar.

But not winning a VBP round does not signal the end for a particular drug product and there are examples showing alternative strategies.

First of all, there is still market space left for companies which didn’t win a bid. The VBP rule requires that if there is only one winner, that company can take 50% of the pooled volume. If there are more than three winning bids, the winners can collectively take as much as 80%, still leaving 20% to non-winning drug makers.

Also, the VBP process only applies to procurement for public hospitals in most but not all of the 31 provinces in China, and patients can still choose to stick to off-patent originators from other channels such as retail or online pharmacies.

The switch from originator drugs to domestic generics thus won’t take place overnight, as the central procurement scheme had hoped. Pfizer, for one, has shown that although it didn’t win the bid in the last round for Lipitor (atorvastatin) and Norvasc (amlodipine), the branded product sales didn’t drop but rather grew, perhaps helped by perceptions of quality.

Pfizer's second-quarter earnings showed that its Upjohn business in China grew by 17% in the three months, driven by the strong performance of the two drugs.

For the latest news coverage on commercial developments in drug pricing from Scrip, ACCESS A 7-DAY FREE TRIAL.